What is retirement income planning?

Retirement income planning is the process of converting your savings, pensions, government benefits, and investments into reliable after-tax income that can support your lifestyle throughout retirement. A comprehensive retirement income strategy coordinates when and how money is withdrawn from accounts such as RRSPs, RRIFs, TFSAs, pensions, and non-registered investments while considering taxes, inflation, investment risk, and estate planning.

Introduction

Imagine two Ontario couples.

Both retire at age 65.

Both have invested diligently for decades.

Both have accumulated $1.5 million in retirement savings.

Both receive similar Canada Pension Plan (CPP) and Old Age Security (OAS) benefits.

On paper, their retirements look almost identical.

Yet twenty years later, one couple has significantly more after-tax wealth, has preserved more government benefits, and feels financially secure.

The other has paid substantially more in taxes, experienced larger mandatory RRIF withdrawals than expected, and worries about whether their savings will last.

What made the difference?

Not investment returns.

Not luck.

Not finding the "perfect" mutual fund.

The difference was how they converted their savings into retirement income.

Accumulating wealth and spending wealth require different strategies.

During your working years, your objective is generally straightforward: save consistently, invest wisely, and grow your assets.

Retirement changes the equation completely.

Instead of asking:

"How much can I save?"

You begin asking:

"How much can I safely spend?"

That single shift changes almost every financial decision you make.

Retirement Is a Distribution Problem, Not an Accumulation Problem

Most Canadians spend 30 to 40 years learning how to accumulate wealth.

Very few spend time learning how to distribute it.

Yet retirement success depends just as much on how you withdraw your money as it does on how you invested it.

Every year in retirement, you must answer questions such as:

How much income do I need this year?

Which account should I withdraw from first?

How much tax will this withdrawal create?

Will this increase my OAS recovery tax?

How should I adjust withdrawals if markets decline?

Should I spend my TFSA now or preserve it for later?

How do I balance today's lifestyle with tomorrow's security?

Each decision influences the next.

That's why retirement income planning is often described as a coordination exercise rather than a series of independent choices.

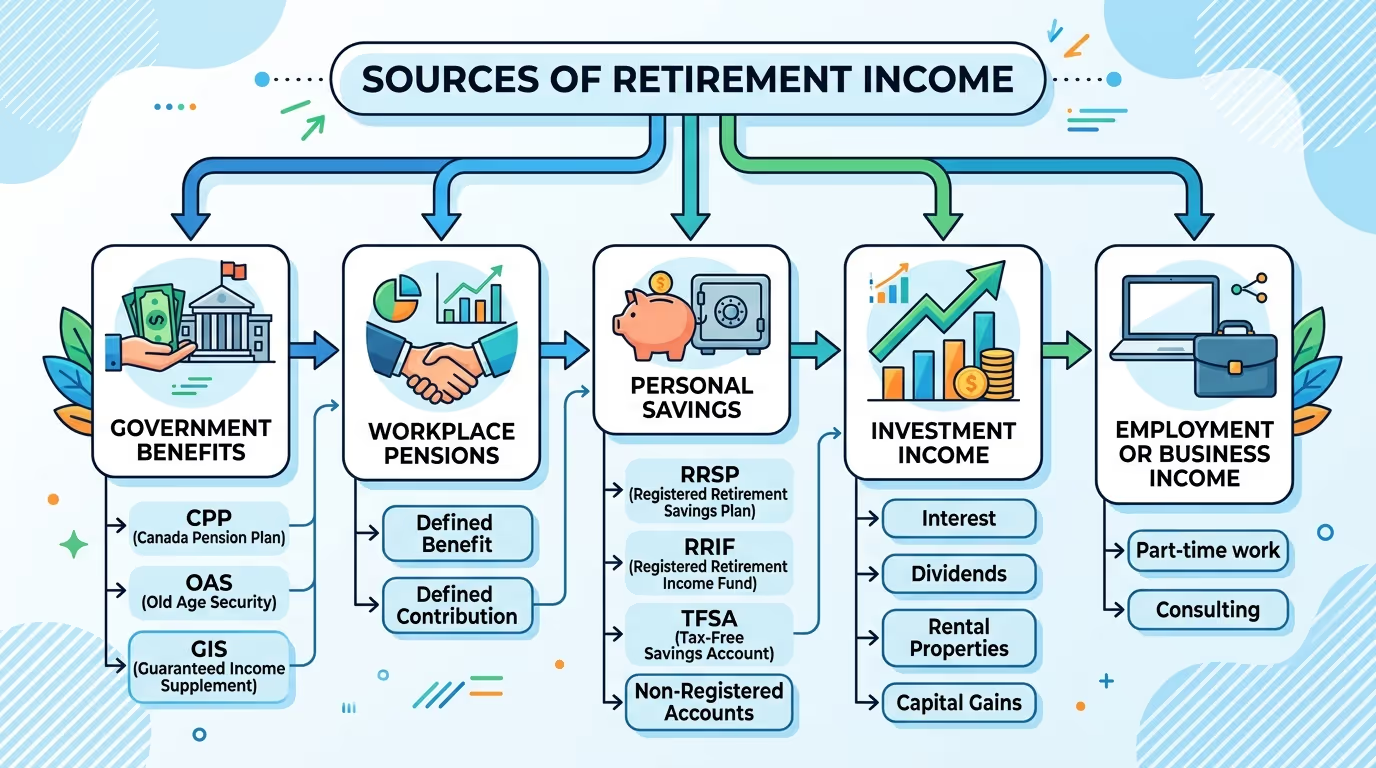

The Five Sources of Retirement Income

Most retirees don't rely on a single source of income.

Instead, retirement income is built from several components, each with its own tax treatment, flexibility, and planning considerations.

1. Government Benefits

For many Canadians, government programs provide the foundation of retirement income.

These may include:

Canada Pension Plan (CPP)

Old Age Security (OAS)

Guaranteed Income Supplement (GIS), where applicable

Planning decisions often focus on when to begin benefits and how they interact with other income sources.

2. Workplace Pensions

Employer-sponsored pensions may provide predictable monthly income throughout retirement.

Questions to consider include:

Should you choose a lump sum or lifetime pension, if offered?

How does pension income affect your tax position?

Can pension income be split with a spouse?

3. Personal Savings

Many retirees draw income from:

RRSPs

RRIFs

TFSAs

Non-registered investment accounts

Each account has different tax rules.

The order in which withdrawals are made can influence after-tax income over many years.

4. Investment Income

Some retirees receive ongoing income from:

Interest

Dividends

Rental properties

Capital gains

Corporate investments

The tax treatment varies depending on the type of income and where it is earned.

5. Employment or Business Income

Retirement no longer always means stopping work completely.

Many individuals choose to:

Work part-time.

Consult.

Operate a small business.

Continue professional practice.

This additional income may improve financial flexibility but should also be considered when evaluating taxes and government benefits.

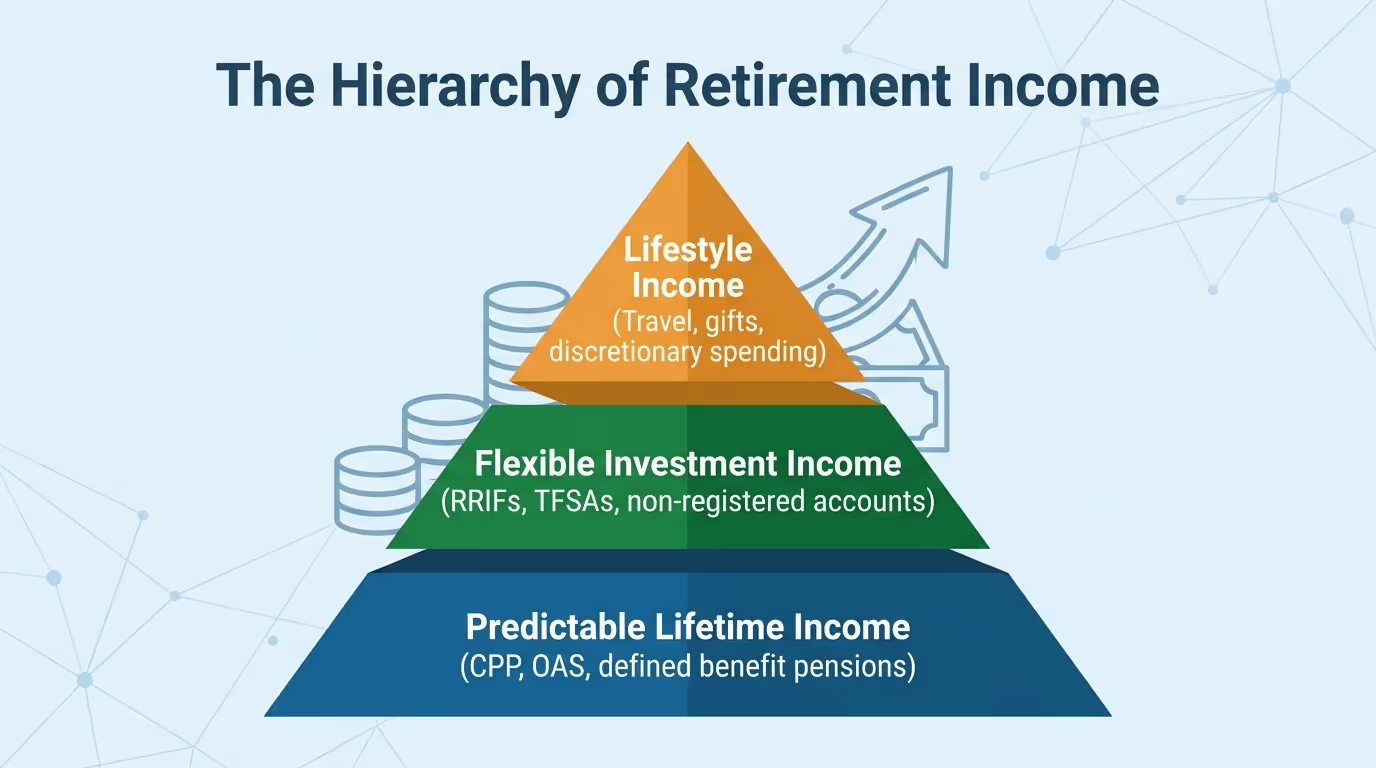

The Retirement Income Pyramid

Rather than thinking about retirement income as one large pool of money, it can be helpful to think of it as a pyramid.

The base provides stability.

The middle provides flexibility.

The top supports discretionary goals.

This perspective helps retirees understand which income sources are dependable and which require ongoing management.

The Four Questions Every Retirement Income Plan Should Answer

A good retirement income plan is less about predicting the future and more about preparing for it.

1. How much income do you need?

This begins with understanding your expected spending rather than simply applying a percentage to your portfolio.

Lifestyle, housing, travel, healthcare, and family support all influence the answer.

2. Where should that income come from?

Different accounts have different tax implications.

Coordinating withdrawals thoughtfully may improve tax efficiency over the course of retirement.

3. How long does the income need to last?

Many retirement plans should consider the possibility of a retirement lasting 25 to 35 years.

Longevity planning is an important part of managing uncertainty.

4. How flexible is the plan?

Retirement rarely unfolds exactly as expected.

Markets fluctuate.

Inflation changes purchasing power.

Tax rules evolve.

A resilient plan allows for adjustments over time.

A Common Mistake

Many people approach retirement by withdrawing money from whichever account seems most convenient.

For example:

Spending non-registered savings until they are gone.

Leaving RRSPs untouched until mandatory RRIF withdrawals begin.

Using TFSAs only as an emergency fund.

In some situations, this approach may be appropriate.

In others, it can lead to larger taxable withdrawals later in retirement or reduce flexibility when tax circumstances change.

The appropriate withdrawal strategy depends on the individual's financial picture rather than a universal rule.

Expert Perspective

One pattern we frequently see is that people devote enormous attention to growing their retirement savings but comparatively little attention to designing the income strategy that those savings will eventually support.

Investment returns matter.

However, retirement outcomes are also shaped by withdrawal sequencing, tax planning, government benefit coordination, and regular review.

Two households with similar portfolios can experience meaningfully different after-tax outcomes because of these decisions.

Where We Go Next

Retirement income planning is the hub of the entire retirement planning process.

To build a complete strategy, we now need to examine each major income source individually:

Canada Pension Plan (CPP)

Old Age Security (OAS)

RRSPs

RRIFs

TFSAs

Non-registered investments

Employer pensions

Corporate assets (where applicable)

Each of these has unique rules, tax implications, and planning opportunities.

Understanding them individually—and then coordinating them together—is what transforms a collection of accounts into a retirement income strategy.